yahoo Press

Forget interest rate cuts – there’s an inflationary shock coming

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

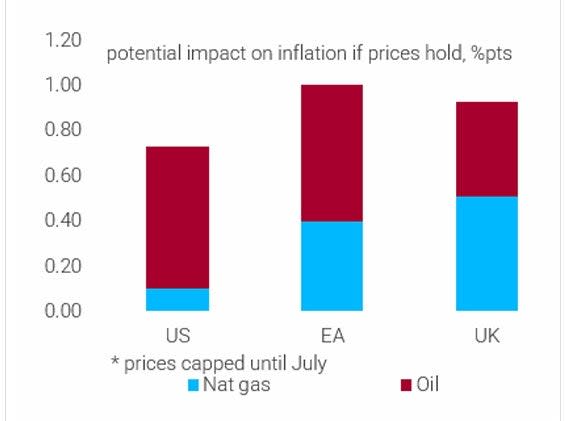

TS Lombard – a GlobalData company (as is Just Auto) – says that an inflationary shock is in prospect due to war in the Middle East, but that the economic impact will not be as severe as the oil shocks of the 1970s. TS Lombard analyst Dario Perkins notes that world market oil prices are up by around 50% and natural gas prices up by more (60% in Europe, 90% in the UK, but less than 15% in the US). That, he says, will feed through into energy-price component of the CPI, but not 1:1. It turns out, he maintains, that the energy component of the CPI is a lot less volatile than the underlying commodities. “Typical DM passthrough is around 20-40%,” he says in a research note. After that, says Perkins, you need to find the weight of oil and natural gas prices in the CPI. “The oil part is easy – the largest part is transportation energy (gasoline for cars etc). Natgas also has its own component. But lots of analysts forget to include electricity. Around 40% of electricity generation comes from natgas, and that will provide an additional inflation boost - eventually.” He sees it as likely around one percentage point contribution or less (below chart). If the war scenario is worse and oil spikes at $150 bbl (a barrel), Perkins calculates that the impact on general prices would be 1.5-2.0 percentage points. “This,” he says, “is not a total disaster, but is going to squeeze real incomes and gives central banks a big headache.” However, he also notes that the current shock would be relatively small, but that the energy intensity of most economies is much lower than it was. “This is nothing like the shocks of the 1970s,” according to Perkins. What should central banks do? Perkins believes that central banks that were already planning to leave rates on hold in 2026 will probably stick to that plan and that hikes are unlikely. “But it’s the central banks that were planning to cut rates [such as the Bank of England] that face the biggest headache. Inflation is already overshooting their targets, and – in their minds – that makes expectations ‘more fragile’”. Perkins finishes his note: “For now, all rates cuts have been postponed.” Implications for automotive markets The latest developments in the Middle East will add weight to demand downside risk as global economic growth is squeezed by higher than previously expected price inflation and interest rates. Consumer and business confidence will take a hit if the war persists. Stock markets have lost significant value already. Any hit to economic growth will negatively impact underlying demand in automotive markets, with associated implications for profitability all along supply chains. Squeezes to real incomes caused by higher than expected price inflation and interest rates will influence purchase decisions as will higher than expected finance costs. There will also be higher costs in materials and manufacturing that will be difficult to pass on to the final consumer, adding to pressures on profitability. Much depends on the trajectory of geopolitical events in the Middle East and their impact on energy markets. A quick end to hostilities with an outcome seen as broadly promoting more stability could lead to a rapid recovery in sentiment and global economic prospects. At the time of writing that seems far from likely. That all said, TS Lombard’s analysis at least suggests that the pending economic shock and its impacts will be less severe than those with long memories might have expected. Central banks and economic policymakers may feel that the eventual magnitude of these additional economic headwinds is most unwelcome - especially in a global macro setting that has struggled to contain inflationary pressures in recent years - but is nevertheless manageable. Another possibility is that higher petrol/diesel fuel prices encourage more fleets and individuals to make the switch to electrified vehicles earlier than would otherwise have been the case. That might prove something of a double-edged sword for many OEM bottom lines though, as they generally make healthier margins on conventional combustion engined vehicles than they do on electrified ones. One confident forecast: More headaches to come. "Forget interest rate cuts – there’s an inflationary shock coming" was originally created and published by Just Auto, a GlobalData owned brand. The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.