yahoo Press

Kontoor Crosses $1B Revenue Mark as Profitability Slips

Images

1 / 4

2 / 4

3 / 4

4 / 4

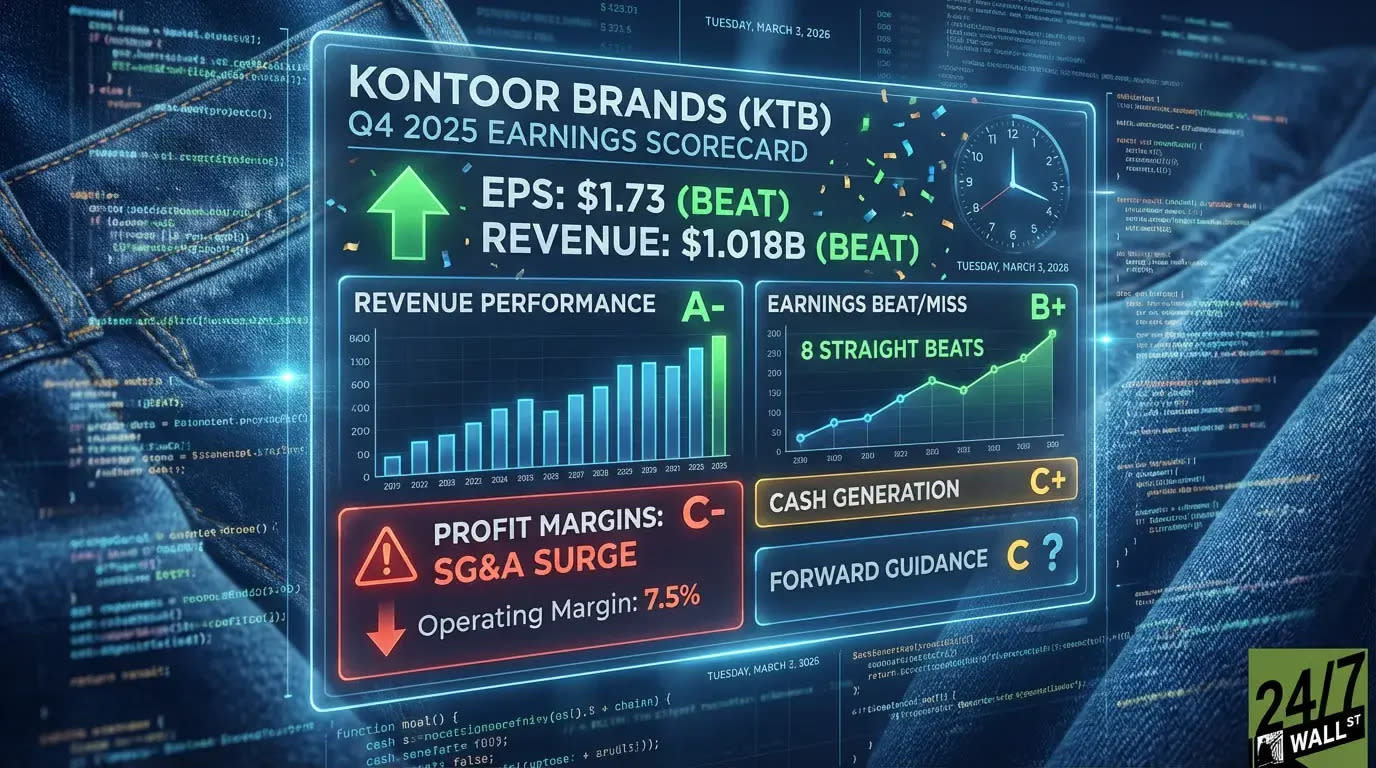

Kontoor Brands (KNG) beat Q4 estimates with $1.73 adjusted EPS and $1.02B revenue. Revenue jumped 46% year over year on Helly Hansen acquisition. Kontoor Brands expanded adjusted gross margin 210 basis points to 46.8% year over year. 2026 guidance projects 9% revenue growth and 15% to 16% EPS expansion. The analyst who called NVIDIA in 2010 just named his top 10 AI stocks. Get them here FREE. Kontoor Brands (NYSE:KNG) delivered a clean double beat to open fiscal 2026, reporting Q4 2025 adjusted EPS of $1.73 against a consensus estimate of $1.67, a +4.85% positive surprise. Revenue came in at $1.018 billion, clearing the $988.8 million estimate by nearly $29 million. Shares were trading at $64.82 heading into today's session, up 6.11% year to date. READ: The analyst who called NVIDIA in 2010 just named his top 10 AI stocks Category Grade Key Insight Revenue Performance A Revenue of $1.018B increased 46% year over year from $699.3M in Q4 2024, reflecting the contribution from the Helly Hansen acquisition along with modest organic growth. Earnings Beat/Miss B+ Adjusted EPS of $1.73 increased 26% year over year and beat the $1.6694 estimate. Reported EPS was $1.31 compared to $1.14 last year. Forward Guidance B Management provided initial full-year 2026 guidance, projecting revenue of $3.40 to $3.45 billion and adjusted EPS of $6.40 to $6.50, representing expected growth of 9% and 15% to 16%, respectively. Profit Margins B- Reported gross margin improved 250 basis points to 46.2%, while adjusted gross margin expanded 210 basis points to 46.8%. Reported operating income rose 44% to $121.1M, and adjusted operating income increased 48% to $150.3M, reflecting improved leverage despite incremental brand investments. Cash Generation B Full-year operating cash flow totaled $455.8M. During the quarter, the company made a $200M voluntary term loan payment and repurchased $25M of shares, reflecting disciplined capital allocation alongside deleveraging efforts. Management Tone B+ Management characterized 2025 as a transformational year driven by the Helly Hansen acquisition, strong Wrangler growth, and disciplined execution. The tone emphasized deleveraging progress and confidence entering 2026. The headline numbers are strong. Revenue surpassed $1 billion for the quarter, increasing 46% year over year, supported by the Helly Hansen acquisition and steady brand performance. Adjusted operating income climbed 48% to $150.3M, and adjusted EPS rose 26%. Importantly, margin performance improved rather than deteriorated. Adjusted gross margin expanded to 46.8%, and adjusted operating margin reached 14.8%, up 30 basis points year over year. At $64.82, the stock trades at roughly 10x forward earnings based on 2026 guidance, a valuation that appears undemanding if projected earnings growth materializes. With initial 2026 guidance calling for high-single-digit revenue growth and mid-teens EPS expansion, the earnings call will focus on tariff impacts, Helly Hansen integration execution, and sustained margin expansion. Wall Street is pouring billions into AI, but most investors are buying the wrong stocks. The analyst who first identified NVIDIA as a buy back in 2010 — before its 28,000% run — has just pinpointed 10 new AI companies he believes could deliver outsized returns from here. One dominates a $100 billion equipment market. Another is solving the single biggest bottleneck holding back AI data centers. A third is a pure-play on an optical networking market set to quadruple. Most investors haven't heard of half these names. Get the free list of all 10 stocks here.